Foreigners living in Japan sometimes pay Japanese taxes, but we assume some people have the following questions.

- When and how do I have to pay for it?

- How is the tax amount calculated?

- What procedures do I have to perform?

In this article, we will explain about income tax, consumption tax, and resident tax that foreigners living in Japan should keep in mind.

Income Tax in Japan

Income tax in Japan is calculated and taxed based on the income earned from January to December. Let’s see how it works.

Calculation of Income Tax

The calculation formula for income tax is as follows.

Income tax = Income × Tax rate

The important point here is the word “income.” It is not equal to revenue. You can calculate your income by the following formula.

Income = Revenue – Income tax deduction

There are 14 types of income tax deductions in Japan, and the deductions applied to vary depending on the person.

- deduction for casualty losses

- deduction for medical expenses

- deduction for social insurance premiums

- deduction for small-scale enterprise mutual aid premiums

- deduction for life insurance premiums

- deduction for earthquake insurance premiums

- deduction for contributions

- deduction for persons with disabilities

- deduction for widows (widowers)

- deduction for working students

- deduction for spouse

- special deduction for spouse

- deduction for dependent

- basic deduction

The deductions applicable to foreigners are basically the same as for Japanese, but there are also differences depending on whether they are “resident” or “non-resident.”

Also, when income is fixed, not only income tax but also the amount of resident tax is decided (we will explain the resident tax later.)

Difference between Resident and Non-resident in Income Tax

Residents and non-residents vary in applicable deductions and the range of income to be levied.

Under the Income Tax Law, a resident is an “individual who has an address in Japan or has a residence (*1) for at least one year up to the present.” Those who do not fall into this category are treated as non-residents.

Also, among residents, those who meet both of the following conditions are “non-permanent residents.”

- The person doesn’t have Japanese nationality.

- The total period of having an address or residence in Japan within the past 10 years is 5 years or less.

Reference: No.2012 居住者・非居住者の判定(複数の滞在地がある人の場合)|国税庁 (Japanese)

Keep in mind that foreigners also become “residents” if they have an address or a residence in Japan for more than a year.

The range of income subject to be levied income tax and the applicable deductions are as follows.

[Scope of imposing income tax]

| Residents | Permanent Residents: All income in Japan and abroad Non-Permanent Residents: All income in Japan and income remitted to Japan (income generated abroad and paid abroad is not taxable) |

| Non-residents | All income in Japan |

Reference: No.2012 居住者・非居住者の判定(複数の滞在地がある人の場合)|国税庁 (Japanese)

[Applicable deductions]

| Residents | 14 income deductions (*2), the same as Japanese |

| Non-residents | Basic deduction, deduction for casualty losses, and deduction for contributions |

Reference: No.1100 所得控除のあらまし|国税庁 (Japanese)

*1 Residence = where you live, but not your home

*2 4 deductions to watch out for:

・Deduction for medical expenses … Medical expenses paid overseas are also included in the deduction.

・Deduction for social insurance premiums … Social insurance premiums paid overseas are basically not deducted. However, certain insurance premiums based on the tax treaty (*3) are deducted.

・Deduction for life insurance premiums … Insurance premiums paid to overseas life insurance companies are not deducted.

・Deduction for dependent … Family members living overseas are also eligible. (Requires documents to prove the fact of remittance)

*3 Tax treaty … A treaty to prevent double taxation between Japan and overseas.

How to Pay the Tax

If you are an employee or a part-timer at a company, your company takes care of paying income tax.

Your company calculates your income tax on your salary and deducts it from your monthly salary. This process is called tax withholding.

Therefore, if you receive a salary from your company, you don’t need to do anything for paying income tax. (*Individuals who meet certain conditions must file an individual tax return.)

If you would like to know how much income tax is deducted from your salary, check your salary statement.

Income Tax Rate and Refund

Income tax in Japan has a system called “progressive taxation.” It is a system that people who have a lot of income pay more taxes accordingly. Many countries adopt the same system.

In Japan, there is a minimum tax rate of 5% to a maximum of 45%, depending on your income. Below is the list of income and tax rates.

| Income amount (rounded down to the nearest thousand yen) | Tax rate | deduction amount |

|---|---|---|

| 1.95 million yen or less | 5% | 0 yen |

| Over 1.95 million yen – 3.3 million yen | 10% | 97,500 yen |

| Over 3.3 million yen – 6.95 million yen | 20% | 427,500 yen |

| Over 6.95 million yen – 9 million yen | 23% | 636,000 yen |

| Over 9 million yen – 18 million yen | 33% | 1,536,000 yen |

| Over 18 million yen – 40 million yen | 40% | 2,796,000 yen |

| Over 40 million yen | 45% | 4,796,000 yen |

*Calculation formula: (income × tax rate) – deduction amount = income tax amount

*The tax rate on domestic income for non-residents is uniformly 20.42%.

If income tax is deducted too much for withholding tax, the difference will be refunded. Although it depends on the company, many companies refund it together with the salary in December or January.

There are various cases of refunds. Let us give you an example.

When you get married before the end of the year, you can use the spouse deduction. This reduces your income, and therefore your income tax. As your company calculated your income tax without spouse deduction, the difference will be refunded.

Consumption Tax in Japan

Consumption Tax System

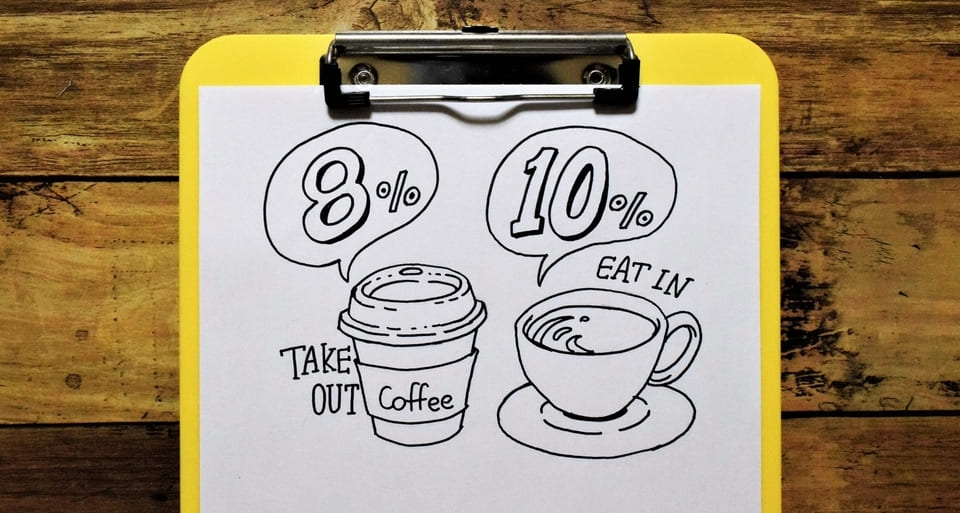

When you buy things in Japan or receive services, you pay the price + consumption tax. The consumption tax in Japan is mainly 8% for food and 10% for other items. (As of May 2020)

The tax rate for food varies depending on whether you take it out or eat it at the store. For example, if you buy food to take home at a convenience store, the consumption tax is 8%, but if you eat it in the eat-in space, it will be treated as eating out (10%).

About Tax-free Shops in Japan

In the streets of Japan, you may find shops that say “Tax-Free.” Unlike Duty-Free shops mainly at airports, this is a shop where you don’t have to pay the Japanese consumption tax when you buy something to send overseas.

What you send overseas is consumed overseas, so Japan’s consumption tax is exempt.

Tax-free shops target non-residents only. Please see below for the target items and conditions.

- General goods … Home appliances, bags, shoes, clothes and kimonos, watches, folk crafts, etc.

- Consumables … Food, beverages, cosmetics, pharmaceuticals, etc.

- General goods … Applicable when you shop at the same store for more than 5,000 yen a day

- Consumables … Applicable when you shop at the same store for more than 5,000 yen and up to 500,000 yen a day

Resident Tax in Japan

Resident Tax System

Resident tax is a tax paid to the area where you live. The following people have to pay:

- Residents with an address in Japan as of January 1 of that year (*4) (non-residents do not have to pay)

- Those who have a certain amount of income (*5) in the previous year

*4: You need to pay it even if you leave Japan on January 2nd.

*5: It depends on the area you live in. In the case of a single person in the 23 wards of Tokyo, it is 350,000 yen (as of May 2020.)

How to Pay the Tax

You will pay the resident tax by either of two methods: general collection and special collection.

- General collection: It is a method of paying by yourself. A payment slip will be sent from the local government that you live in around June, so you will have to pay in four parts. (June, August, October, next January)

- Special collection: This is the method that the company pays on your behalf. The resident tax amount will be deducted from your monthly salary.

If you are a company employee or a part-time worker, most of the cases, it will be a special collection.

Resident Tax Rate

The resident tax consists of an income-based portion and a per capita portion.

- Income-based portion: Pay according to the previous year’s income. (10% in principal)

- Per capita portion: Pay a fixed amount. (*There are regional differences, for example, Tokyo 23 wards → 5,000 yen, Kyoto → 5,600 yen)

The amount determined here is the resident tax payment amount for one year. In the case of general collection, you are paying it in four times, and in case of the special collection, your company will deduct it from the monthly salary.

Conclusion

We have explained three taxes you may need to know. If you are working, your company will take most of the necessary procedures, so don’t worry.

If you would like to know more in detail, it’s also a good idea to ask the person in charge of it in your company.